The nature of how and where Americans spend their hard-earned dollars continues to be in flux. Early in the era of COVID-19, cooped-up households went all in on home improvement products and sporting goods. In 2022, “revenge spending” took over as experiential retail and travel blossomed.

How and where money is spent, naturally, is closely related to current economic and lifestyle conditions. Inflation has eaten away at purchasing power, but the labor market remains tight and households are still willing to shell out more money, even if it doesn’t get them more stuff. One theory regarding this consumer stubbornness is that revenge spending has been replaced by “retail therapy.” In other words, as long as the job market doesn’t fall off a cliff, consumers will continue to purchase goods and services in rebuke of their large-scale concerns for geopolitical strife, climate change and other issues.

This is an intriguing hypothesis that certainly impacts the retail sector’s near-term commercial real estate prospects. Given the prevailing crosswinds in retail, the Moody’s Analytics forecast for 2023 currently calls for subtle rent growth and few changes to occupancy rates (similar to 2022 performance).

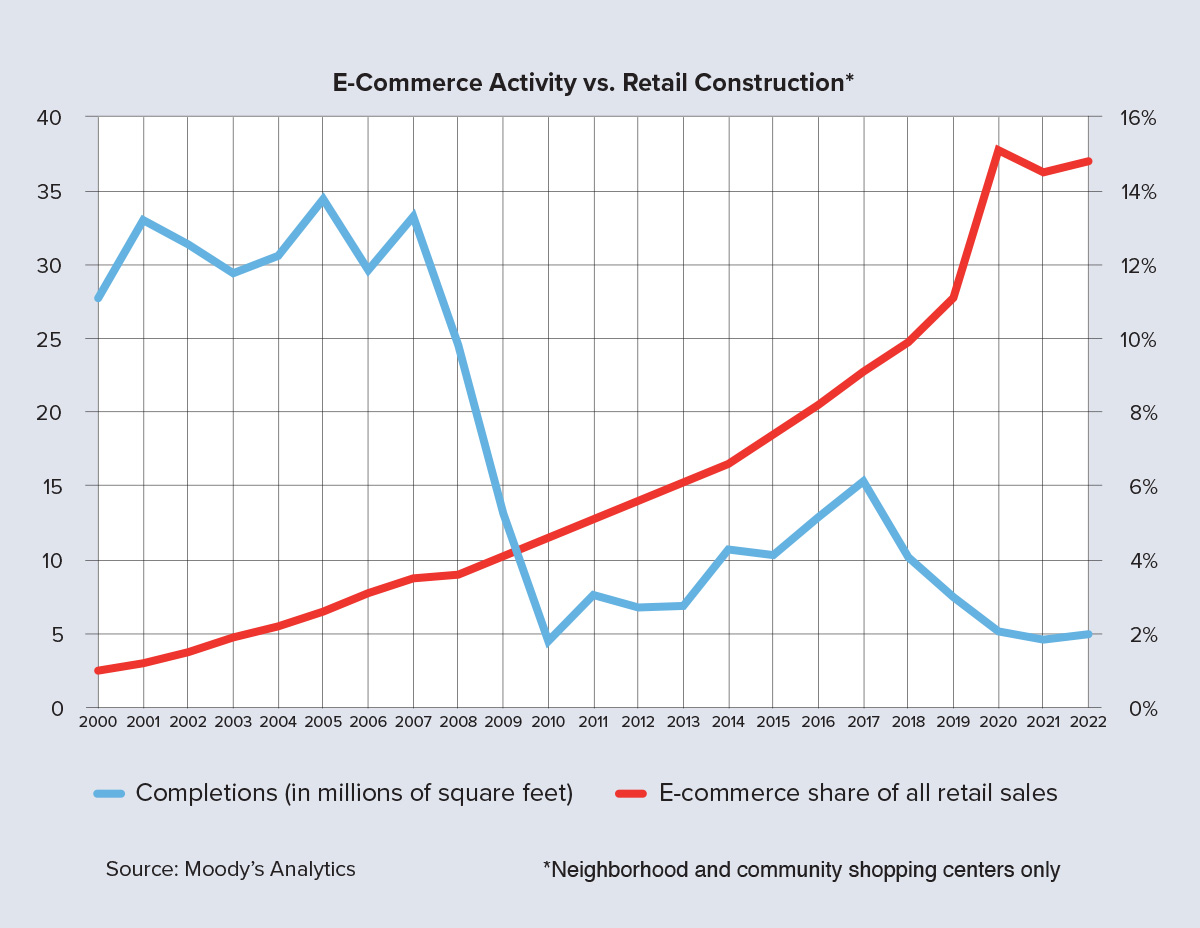

But what about the longer-term prospects for the sector? How are consumer spending habits shifting the priorities and activities of developers and investors? If we look back over the prior two decades, we see a dramatic shift in retail construction activity. As the chart on this page shows, the growth of big-box and discount retailers pushed nationwide inventory growth for neighborhood and community shopping centers to about 30 million square feet per year prior to the Great Recession. When the economy went south, completions dropped significantly for a few years.

A mild recovery occurred prior to the pandemic, but activity barely approached half of its previous levels. A fundamental change in stakeholder expectations for brick-and-mortar stores had occurred. Speculative construction declined dramatically and was replaced by thoughtful developments, renovations and repurposing of existing space. A rightsizing of the sector had commenced.

Like the Great Recession before it, the shock of the pandemic has only served to accelerate this rightsizing. This time, however, it wasn’t a performance decline as much as an e-commerce acceleration that frightened developers. The data chart shows that e-commerce has not permanently blossomed as much as some expected early in the pandemic, but its share of all retail spending is still significantly higher than in 2019 and is likely to continue growing, possibly reaching 20% later in this decade. Consequently, retail-sector development is now at its lowest point in decades, a trend that is unlikely to change soon.

Not all is dire, however, for the sector. Omnichannel retail — which mixes online distribution, pickups and returns with in-person shopping — is here to stay. Responding to this trend, developers have shifted their interest toward lifestyle-type centers. Retail is increasingly being added near existing apartments, or vice versa, and there are many new walkable mixed-use projects being constructed across the country. This style is theoretically a win-win for all parties involved. Residents get easy access to shops and social opportunities while retailers get a consistent level of foot traffic. Office, medical and wellness spaces have been brought into many of these developments, further increasing the potential consistency of patrons and creating a critical mass that retail needs for success.

Examples of this master-planned style of development aren’t entirely new. The massive Legacy West project in Plano, Texas, and North Hills in Raleigh were built prior to the pandemic. Nonetheless, the pace of this trend is picking up quickly, with particularly popular models involving a repurposing of troubled Class B and C mall space.

So, while the currently weak development numbers may paint a picture of a sector that many believe to be severely troubled, this emerging retail evolution will provide many intriguing opportunities in the coming years. Retail continues to evolve, as it always has, but this time around it needs a good deal of rightsizing and repurposing. ●