As we approach the end of the year, there are precious few opportunities left to acknowledge the hard work of Scotsman Guide’s 2023 Top Originators. The top-producing women originators, those who served in the military, under-40 standouts and more were recognized this year. But for this penultimate ranking, we’re returning to the numbers underneath it all.

The following pages contain the Top Purchase Volume and Top Refinance Volume rankings. These lists highlight the top 100 salespeople for purchase volume, as well as the top 100 for refi volume, based on 2022 production reports. As with each of this year’s previous rankings, sales numbers are down across the board compared to 2022 data, which measured 2021 production. As the housing and mortgage markets have dipped and normalized since the post-pandemic boom, Scotsman Guide’s rankings have reflected it. But these numbers are not historically low by any means. This year’s Top Purchase Volume rankings exceeded figures from the 2021 list, both in aggregate volume and top individual volume.

Shant Banosian of Guaranteed Rate is at No. 1 in the Top Purchase Volume rankings for a fifth year in a row. His purchase volume has steadily increased over the years, peaking in the 2022 rankings at more than $1 billion. If last year is treated as an outlier, however, Banosian is still on an upward trajectory, having increased his purchase volume from $477.4 million in the 2019 rankings to $815.8 million this year.

Second in this year’s Top Purchase Volume rankings is Mark Cohen of Cohen Financial Group, who similarly increased his purchase volume from $396.7 million in the 2021 rankings to $578.2 million this year. Cohen also moved up two spots in this year’s rankings after a fourth-place finish last year. He’s followed by Ben Cohen of Guaranteed Rate ($550.9 million), whose purchase volume jumped $160 million from the 2021 rankings, and Matt Weaver of CrossCountry Mortgage ($520.4 million), who posted a gain of $185 million from two years ago.

The Top Refinance Volume rankings are a little more complex. While many consider 2020 and 2021 to be the refi boom years, the surge actually began in 2019, when 30-year fixed rates dipped below 4%. In August 2019, refinances had doubled from the previous year, according to data from the Mortgage Bankers Association. Now that the boom has passed, the rankings look much like those published in 2019 based on 2018 origination volumes — impressive when considering that the average mortgage rate in 2022 was almost 1% higher than in 2018.

While there are a couple of familiar names in the top five, this year’s Top Refinance Volume rankings saw dedicated refi originators jump up the list dramatically. Hank Metzger of American Financing Corp. took the top spot for 2023, up 10 spots from last year, with a refinance volume of $239.7 million. Notably, 100% of Metzger’s business in 2022 came via refinances. He’s followed by Damon Germanides of Insignia Mortgage ($184.4 million), who increased his refi volume by $26 million and placed No. 2 after not finishing among the top 100 a year ago.

Germanides is followed by Mark Cohen ($173.2 million), who rose nine places from last year; Daniel Klein of Century Capital Partners ($170.7 million), who is new to these rankings; and Thuan Nguyen of Loan Factory Inc. ($156.3 million), who was No. 1 on the Top Dollar Volume and Top Refinance Volume lists in 2021 and 2022.

Congratulations to everyone who earned a place in this month’s rankings. In a difficult year, you outdid yourselves despite a significant disadvantage with interest rates. Keep an eye out next month for the final 2023 Top Originators ranking, State Champions. Have a happy Thanksgiving and a wonderful start to your holiday season, and as always, thank you for reading.

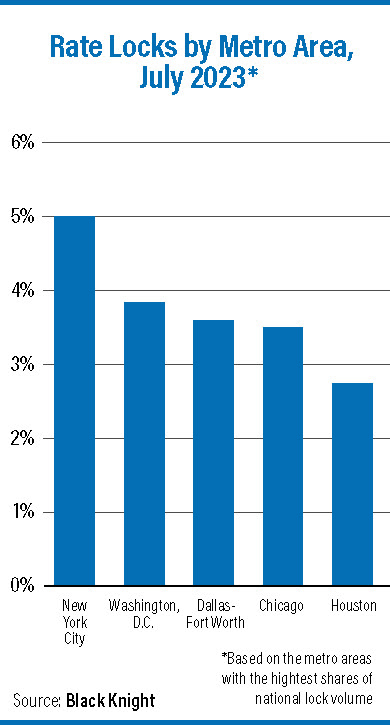

Rate locks drop as credit tightens

This past July, interest rates for 30-year conforming loans rose above 7% for the first time since spiking in November 2022. This caused a drop in mortgage demand, according to Black Knight’s Originations Market Monitor report, despite a decrease in rates by the end of that month.

Overall rate lock volumes were down 7% from June to July. Purchase loan locks made up the lion’s share of rate locks at 88% but were still running well below July 2022 levels. On a year-over-year basis, purchase locks were down 27%, and they were down 35% from pre-pandemic levels in 2019. The average purchase price also dropped slightly from its peak in June, receding to $456,000.

According to Black Knight, signs of credit tightening were seen in July’s rate-lock data through rising downpayments, higher credit scores and lower loan-to-value ratios. Average credit scores on purchase locks for primary residences hit a record high early in July before edging downward.

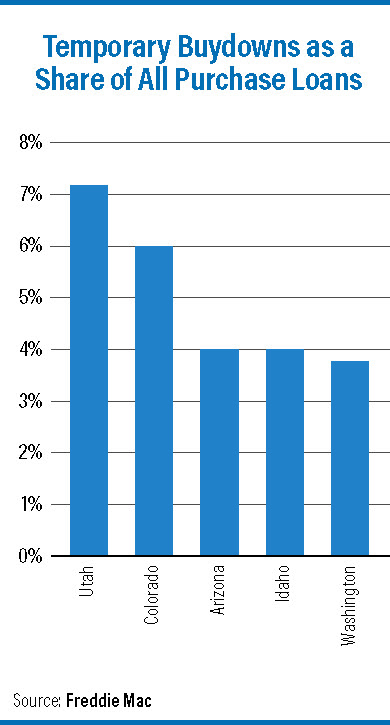

Temporary rate buydowns drop from recent peak

Mortgage rate buydowns gained popularity in 2022 as interest rates rose, allowing new homeowners to temporarily reduce their rate for a period of one to three years. In December 2022, buydowns peaked at 7.6% of all Freddie Mac-funded loans, according to a report from the government- sponsored enterprise.

But the most recent data available, in June 2023, found only 2.8% of loans with buydowns. This still represents an increase from the near-zero levels of buydowns in early 2022.

Buydowns remain a very niche market, according to the report. They’re clustered both geographically and by lender as 12 nonbanks accounted for 80% of all buydowns in June. Western states had significantly more buydowns, led by the likes of Utah, Colorado, Idaho and Arizona. On average, mortgage buydowns comprised about 1% of all loans in Eastern states, while shares in Western states tended to be in the 3% to 4% range, with Colorado (6%) and Utah (7.1%) as outliers.

Buydowns appear to have a trade-off for homeowners, according to Freddie Mac. While these homeowners pay less for the first few years of their loan, their interest rates were 15 basis points higher on average, meaning they could pay more over the life of their loan if they don’t refinance or move.

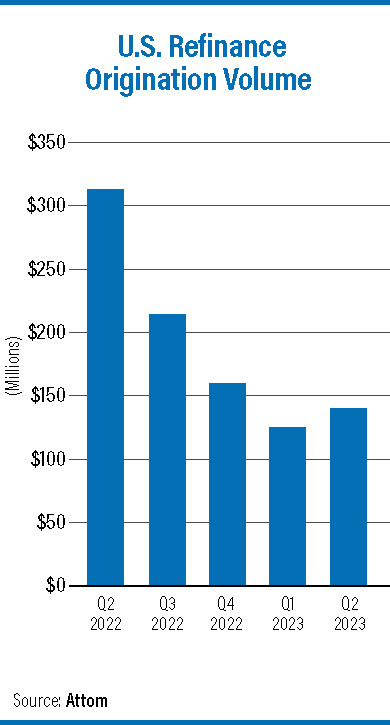

Refinances rise after eight straight quarterly declines

Mortgage origination activity rose across the board in second-quarter 2023, according to Attom. The total number of mortgages issued increased to 1.56 million during these three months. While still representing a decrease of 38% from Q2 2022, originations rose 21% from Q1 2023, ending eight straight quarters of declines.

Despite a slight rise in interest rates in Q2 2023, improvements were seen in the purchase, refinance and home equity markets. Purchase loans jumped by 29%, refinances by 14% and home equity lines of credit (HELOCs) by 13%.

Notably, the rebound in refinances came after the market posted a record-low total in Q1 2023. From April through June, lenders issued $141 billion in refinances across 477,219 loans, with units up 14% and volume up 8% from the prior quarter. Refis improved in 90% of U.S. metros analyzed, with the largest quarterly increase in Knoxville, Tennessee (up 87.4%). Refis accounted for 30.7% of all originations in Q2 2023.

HELOCs also increased after two straight quarters of declines. In the second quarter, lenders originated $50.9 billion in HELOCs across 284,591 loans. HELOCs made up 18.3% of all loans during these three months, down from 19.6% in the prior quarter but still four times higher than the levels of early 2021.

Midwest states lead in affordable single-family rentals

Although homeownership is temporarily out of reach for many Americans, many families still want to live in single-family homes. While this tends to be a more expensive option than an apartment, there are still many U.S. markets where this can be achieved affordably, especially due to the growing trend of built-to-rent homes.

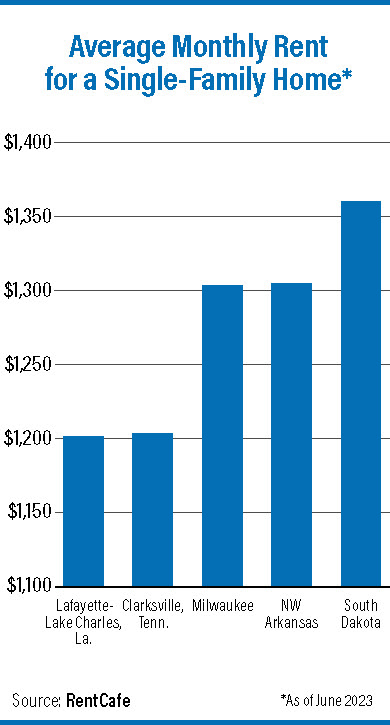

An August 2023 report from RentCafe found that 20 markets across the country had single-family homes with average rents of less than $1,700. Of these metro areas, about half were priced below $1,500, on average.

The Midwest accounted for eight of these 20 markets. Milwaukee ranked No. 3 overall, posting an average rent of $1,317 for a single-family home in June 2023. Indianapolis was 15th, with average rents of $1,628.

The cheapest market was Lafayette- Lake Charles, Louisiana, at $1,203, followed by Clarksville, Tennessee, at $1,213. The states of North Dakota, South Dakota and Montana were listed, while Arkansas, Kansas and Indiana each had two cities that made the cut. Major metros on the list included Pittsburgh; Oklahoma City; Columbus, Ohio; and Las Vegas.