The distressed-property niche of the residential real estate market is typically thought of as a lagging indicator of the overall housing market and the broader U.S. economy, but at least one slice of this niche acts as a leading indicator for the broader housing market, according to an analysis of proprietary data from Auction.com.

This forward-looking piece of the distressed market is the rate of homes sold to third-party investors at public foreclosure auctions. Auction.com accounts for nearly half of these sales nationwide, equating to more than 434,000 properties brought to these auctions over the past seven years. Historically, much of the foreclosure-auction process has been conducted offline, but it is now being digitized to allow for the capture of auction-data metrics that previously never existed.

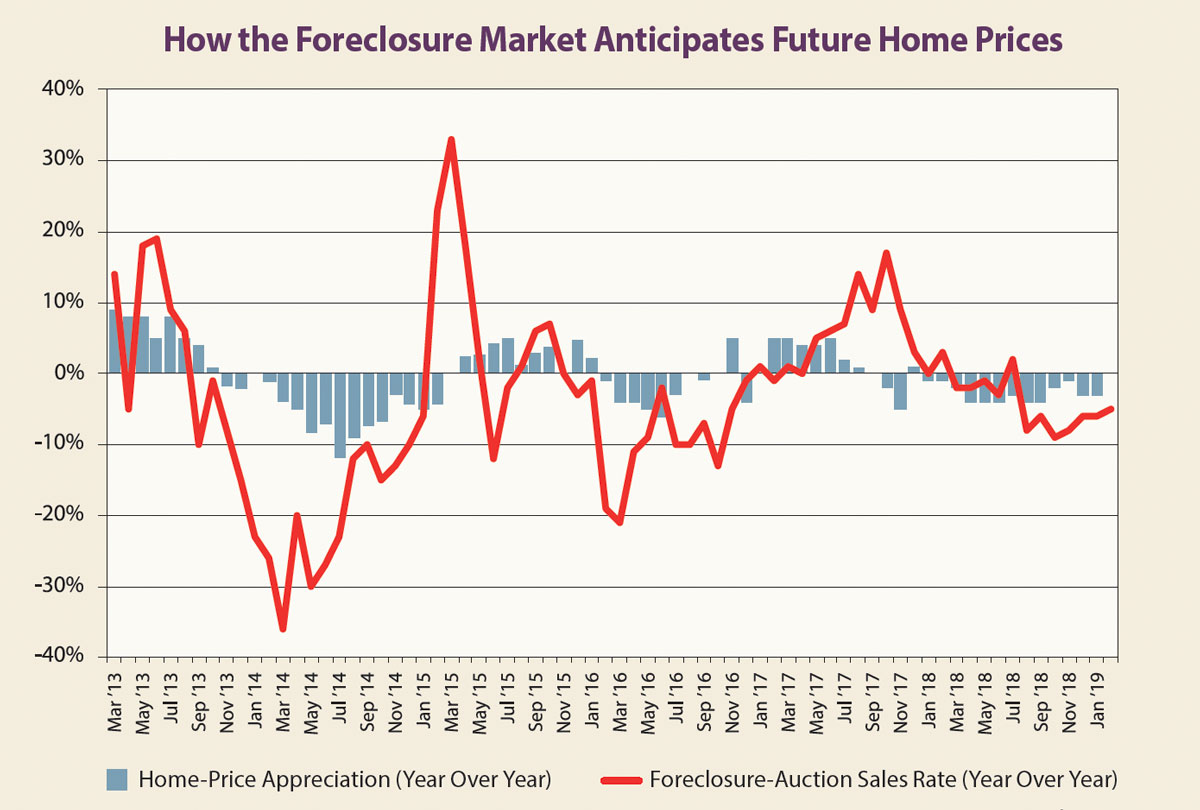

We analyzed the rate of homes sold to investors at public foreclosure auctions from January 2012 to February 2019 and compared it to home-price appreciation data during the same period. Our analysis found that a slowdown in the foreclosure-auction sales rate typically precedes — or, at least, closely parallels — a slowdown in home-price appreciation for the retail housing market. Conversely, a pickup in the foreclosure-auction sales rate typically precedes a rise in home-price appreciation for the retail housing market.

The first example of this pattern occurred starting in September 2013, when the foreclosure-auction sales rate dropped 10 percent. This year-over-year sales-rate decrease continued for 17 consecutive months, ending in January 2015.

Meanwhile, home-price appreciation in the broader market was still accelerating in September 2013, according to Attom Data Solutions. At that time, the U.S. median home price was up 12.1 percent from a year earlier, significantly higher than the 8.6 percent annual appreciation rate in September 2012. But home-price appreciation began to slow in November 2013 — two months after the slowdown in the foreclosure-auction sales rate. That deceleration in annual home-price appreciation continued for 16 straight months through February 2015, reaching a low point of 3.4 percent in July 2014, Attom reported.

Even as home-price appreciation continued to decelerate in February 2015, the rate of investor sales at foreclosure auctions took a dramatic turn and jumped 23 percent year over year. This upward trend continued for the next three months and for six of the next eight months. In this case, decelerating home-price appreciation followed the pullback in foreclosure-auction sales by one month, posting a small increase in March 2015. Home-price appreciation then increased on a year-over-year basis for the next seven months.

Investor behavior at foreclosure auctions also preceded a mild slowdown in home-price appreciation in 2016. The foreclosure sales rate decreased on a year-over-year basis for 13 consecutive months starting in December 2015. Home-price appreciation then decelerated year over year for six consecutive months starting in February 2016 — two months after the downward trend began in the foreclosure-sales rate.

After picking up in 2017, the rate of third-party foreclosure sales flattened out in January 2018 and began a four-month downward trend starting in March 2018. And, after a one-month reprieve in July 2018, the rate dropped for seven consecutive months ending in February 2019. In this case, decelerating home-price appreciation in the retail market actually preceded the slowdown in the foreclosure-auction sales rate. A string of 12 consecutive months of decelerating home-price appreciation began in January 2018.

This analysis shows that investor demand for distressed properties typically either precedes or parallels a corresponding trend in the broader housing market. This is because investors are on the front lines of residential real estate and often have an investment strategy that relies heavily on accurately anticipating short-term market trends, such as the six to 12 months that it takes to rehabilitate and resell (or rent) a property. The analysis also demonstrates that demand in the distressed-housing market can provide useful, forward-looking insights into more widespread housing trends.