Completed foreclosure auctions are steadily returning despite sweeping moratoria measures enacted days after the COVID-19 pandemic declaration this past March — measures that have been extended through the end of 2020.

These moratoria prohibit foreclosures on the vast majority of single-family homes with mortgages backed by the Federal Housing Administration (FHA) and the Federal Housing Financing Agency (FHFA), which oversees Fannie Mae and Freddie Mac. Mortgages backed by these agencies together account for more than 60% percent of all active U.S. mortgages.

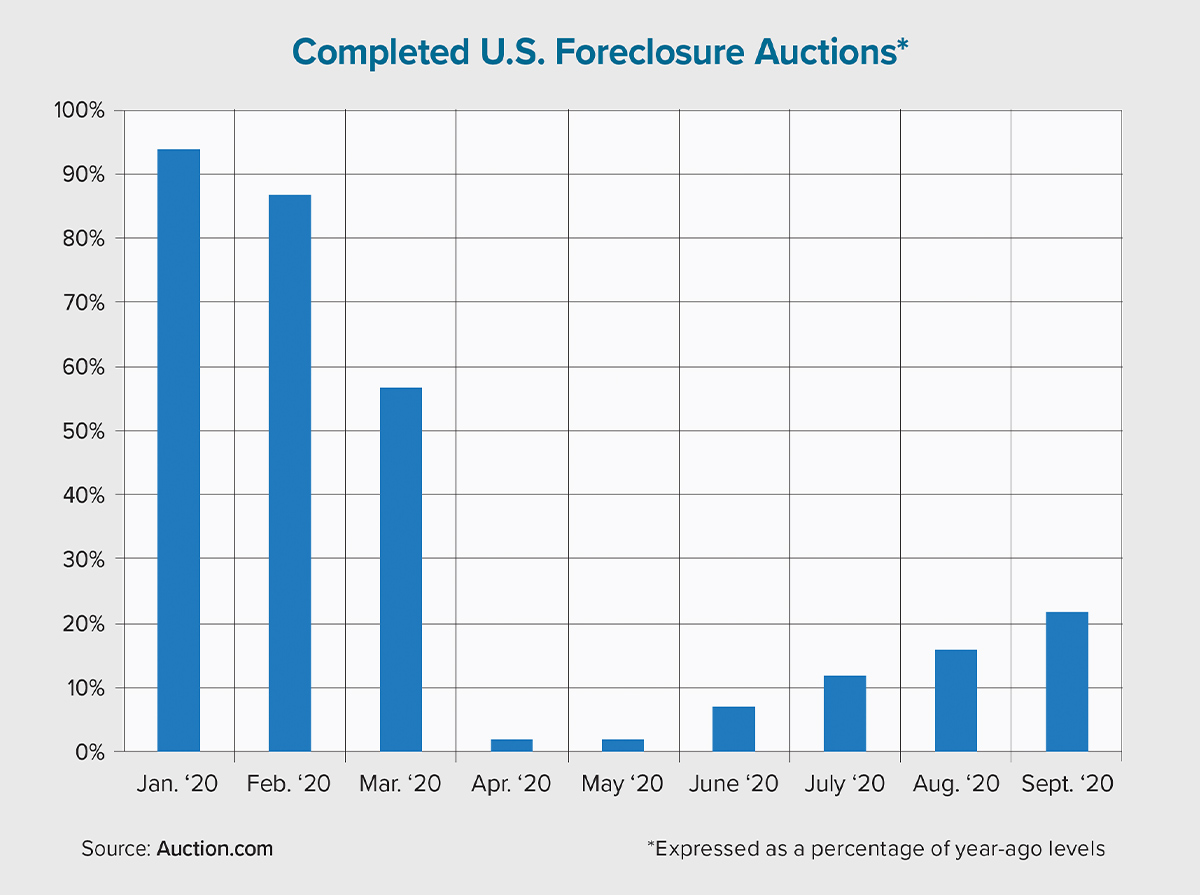

Despite these aggressive and worthy efforts to prevent gratuitous foreclosures during the pandemic-triggered economic crisis, foreclosures increased to a six-month high in September 2020, according to proprietary data from Auction.com. Properties brought to foreclosure auction this past September — meaning the properties either sold to a third-party buyer or reverted back to the foreclosing lender as real estate owned — increased by 24% from August 2020 and were up by more than 1,000% from their post-pandemic low this past April.

Although foreclosures have jumped significantly from their post-pandemic valleys, it’s important to note that they are still well below year-ago levels. The six-month high this past September was 78% lower than September 2019 levels, according to Auction.com data. Still, the steady increase to a six-month high in September begs the question: How are foreclosures increasing in the face of a broad foreclosure ban? The answer lies in an important exemption — vacant or abandoned properties — included in both the FHA and FHFA moratoria rules.

Virtually all properties now being foreclosed upon are vacant or abandoned. The steady increase over the past few months was the result of two factors. First, mortgage servicers have improved the process of identifying properties as vacant or abandoned. Second, more properties that secure delinquent mortgages have become vacant or abandoned as the moratoria have been extended. The second factor is evident in a recent report from Attom Data Solutions that shows the rate of vacant “zombie” foreclosures increased to a three-year high in third-quarter 2020.

Policymakers demonstrated foresight by embedding the vacant- or abandoned-property exception in the moratoria, according to Julia Gordon, president of the National Community Stabilization Trust. Her nonprofit organization focuses on promoting homeownership in distressed neighborhoods. “You want the right tool for the job and stopping the foreclosure process as a whole for every property — especially for vacant properties — is not the right tool,” Gordon said, pointing to the rise in zombie foreclosures in the aftermath of the Great Recession. “When a property is abandoned but does not go through foreclosure in a reasonable period of time, it will invariably blight the community.”

In this context, states in the most danger of unintended negative consequences as the result of vacant foreclosures in the aftermath of the current recession are those in which foreclosure auctions continue to flatline. This past September, there were no foreclosure auctions in seven states, including New York, Oregon and Utah, according to Auction.com data. In the same month, foreclosure auctions were at least 90% below year-ago levels in five other states: Massachusetts, Washington, Idaho, Nevada and Montana.

Meanwhile, states with the largest rebounds in foreclosure auctions at that time included Missouri, Alabama, Arkansas, Arizona and Indiana — all of which posted September 2020 numbers that were at least one-third of year-ago levels. States with the most completed foreclosure auctions at that time were Ohio, Illinois, Florida, Alabama and Texas.

Rather than acting as a warning, however, the steady return of foreclosures acts as a harbinger of long-term health for local housing markets. In many states, vacant foreclosures are being more efficiently renovated and reoccupied. Conversely, in states with a more anemic rebound in foreclosure auctions, vacant properties are more likely to be languishing in foreclosure limbo. This potentially drags down neighborhood values and represents a growing backlog of deferred distress that could disrupt home-price appreciation when it eventually hits the market. ●