Among the core commercial real estate sectors, hotels have arguably experienced the largest disruption since the start of the COVID-19 pandemic. While office and retail have not gone unscathed by any means, the long-term nature of the lease structures in these sectors have meant steadier income streams for office and retail landlords.

With the loosening and elimination of many COVID-related restrictions by the second half of 2021, hotels performed well in the summer months as lockdown fatigue set in and travelers craved changes of scenery. Still, with the delta variant and other strains of the virus emerging by the end of a busy summer travel season, the number of air travelers as measured by the Transportation Security Administration (while maintaining the usual seasonal-demand trends associated with the spring and summer months) leveled off at a rate that was about 30% lower than the same period in 2019.

So, what does this combination of factors mean for the hotel industry in the autumn and winter months? Traditionally, business travel picks up after Labor Day whereas leisure travel tapers off as part of expected seasonality patterns. But as companies, particularly tech giants, continue to reassess return-to-the-office plans, the likelihood of business travel making up the difference in overall travel numbers as it has in years past is diminishing.

Despite this, there was still end-of-summer optimism among potential business travelers. A survey conducted by the U.S. Travel Association in August found that 77% of respondents were willing to travel, given the current conditions. But only 35% of businesses reported that they would resume domestic travel before the holiday season. Vacation travel also seems to be softening beyond the typical cyclicality.

The softness in this area is most evident in the August 2021 labor report as total nonfarm payroll employment grew by 235,000 jobs, well below the consensus forecast of 720,000 jobs. This was due in part to flat job growth in the leisure and hospitality sector, despite it being a main employment driver during the first half of the year.

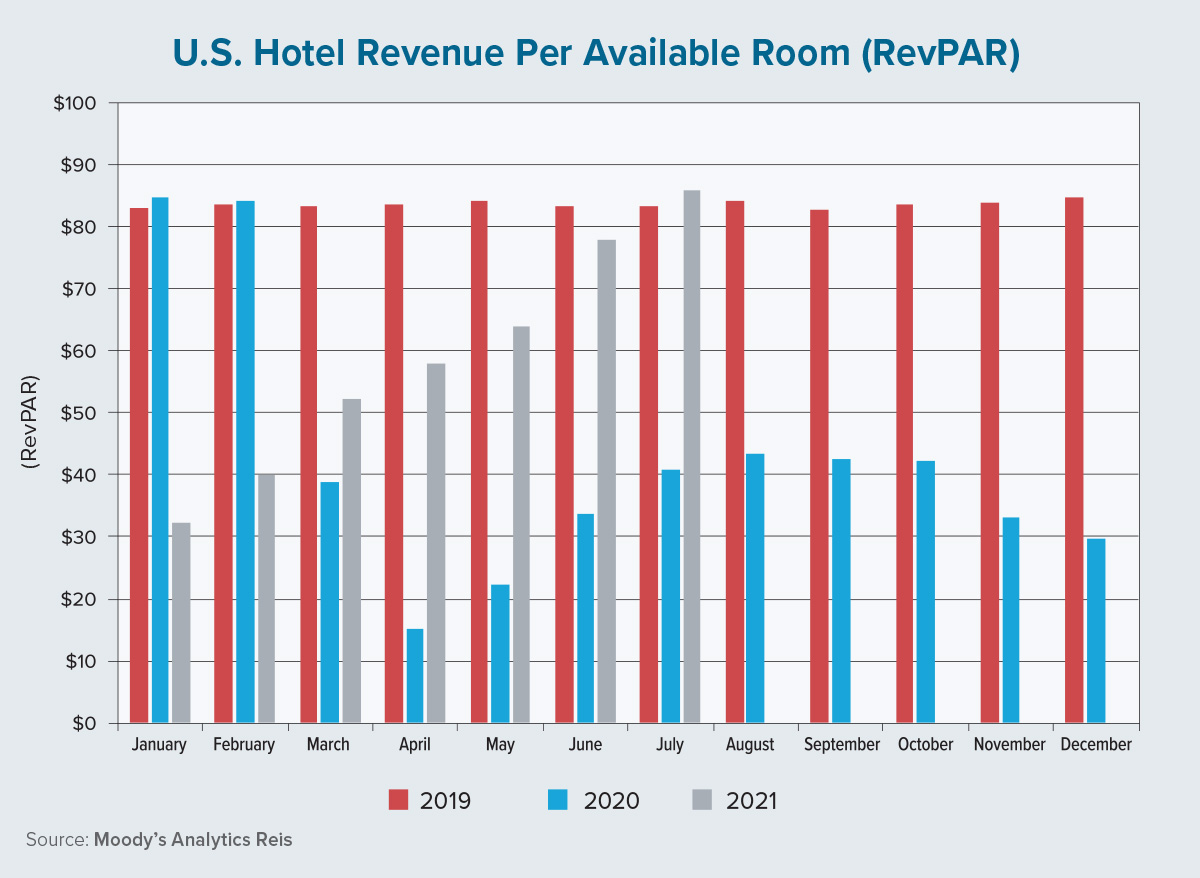

One key indicator of the vitality of the hotel sector is revenue per available room (RevPAR). The accompanying chart illustrates RevPAR’s movement from 2019 to the most recent available data for 2021. In 2019, U.S. RevPAR as a blended average across all tiers of hospitality properties was consistently between $82 and $85 for the entire year, with a monthly average of $83.58.

Last year started off strong — if not slightly stronger — than the opening months of 2019, but hotel performance declined dramatically as lockdowns ensued. In the second half of 2020, however, recovery was visible. It was followed by a decline late in the year as infections surged and business travel remained on pause. The story in 2021 has been much more positive, with a sharp increase in RevPAR over the first seven months of the year.

This past July, RevPAR slightly exceeded 2019 levels in the best sign yet that the hotel sector is making a robust recovery. Despite the uncertainty surrounding travel in the final months of the year, Moody’s Analytics Reis expects stability or only a modest downward shift in RevPAR for the remainder of 2021. As long as public health trends positively in 2022, RevPAR is anticipated to meet or exceed 2019 levels and continue growing throughout the rest of this decade.

Nonetheless, transaction activity in the leisure and hospitality space continues, particularly across resort properties. The focus of leisure travel has shifted heavily in favor of these locations as travelers are seeking out larger-scale properties. Simply put, leisure travelers have eschewed larger cities in favor of vacations that afford more space in a bid to go on holiday while still taking precautions.

Properties located in lucrative big-city markets such as Washington, D.C., also are trading (albeit at a discount) while assets in other large metros, such as Chicago, are actively marketing themselves to potential buyers. Only time will tell when properties whose owners wish to sell will experience capital-market distress due to burdensome debt service in the event that COVID-19 reduces the appetite for travel. ●