Editor’s note:

CoreLogic chief economist Frank Nothaft’s column has appeared in Scotsman Guide for years. It is with sadness to report that he unexpectedly died during production of our July magazine. Read about the loss here.

The Atlantic hurricane season runs from June through November of each year. Recent years have seen an increase in the number of severe storms along with resulting property damage and personal injury. And experts are predicting an above-normal number of tempests again this year. A look back at three storms over the course of 2020 and 2021 show the effects that these storms can have on local housing markets.

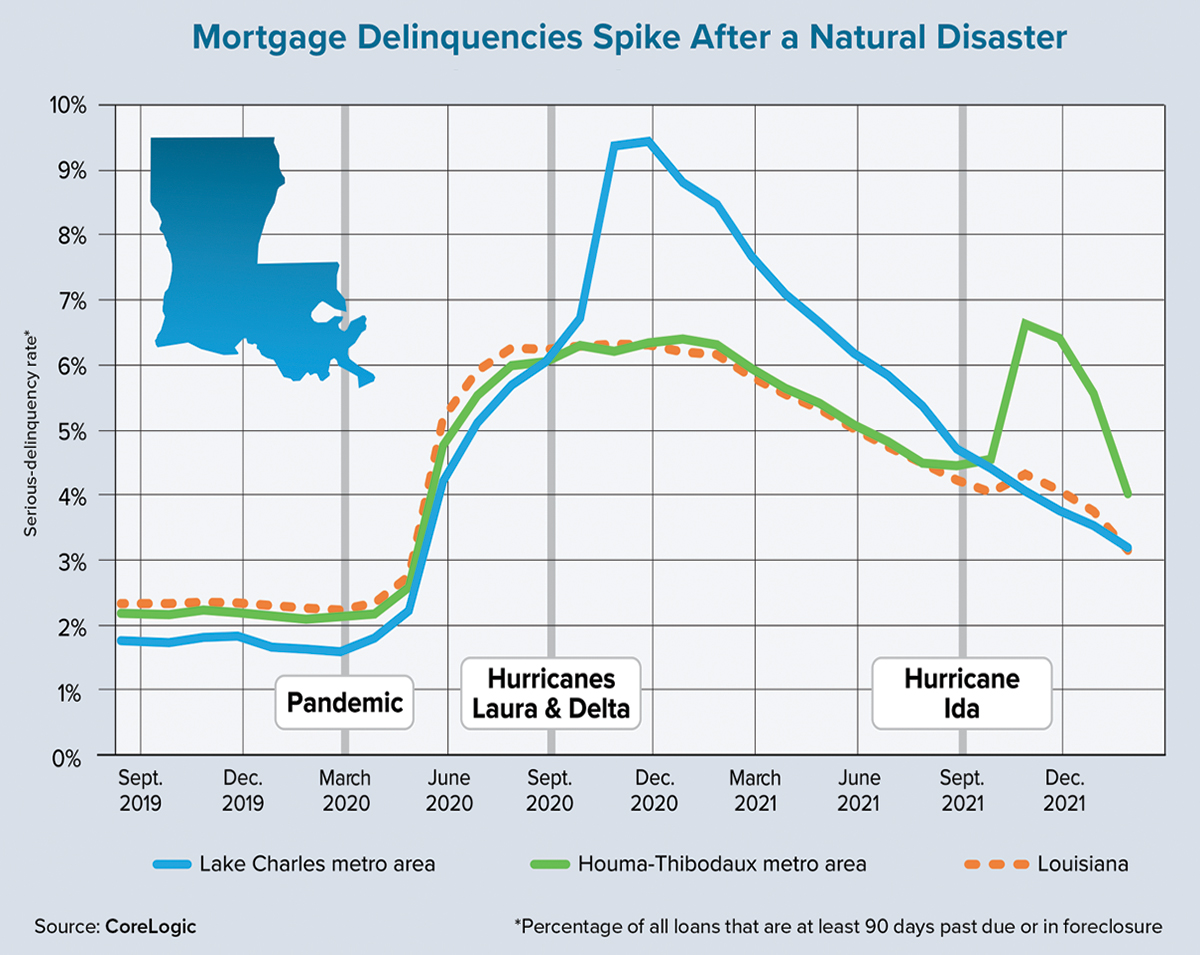

Hurricane Ida, which made landfall in August 2021, was a Category 4 storm that caused nearly 100 deaths and an estimated $75 billion in property damage, with about two-thirds of the damage occurring in Louisiana. Ida made landfall in Lafourche Parish, part of the Houma-Thibodaux metro area. Homes and businesses were damaged or destroyed, and families were displaced. The financial hardship caused by Ida led to a spike in home loan delinquencies. In the month following the hurricane, the transition rate from current to 30-day delinquency status, which had been running at about 1% per month, spiked to more than 7% in the Houma-Thibodaux region, according to CoreLogic data.

Many homeowners experienced ongoing financial trauma. The share of borrowers in Houma-Thibodaux who were at least 90 days behind on mortgage payments jumped by 50% in the latter half of 2021, rising from 4.4% in September to 6.6% in November. This coincided with a 16% decline in the nationwide serious-delinquency rate during the same period. Six months after Ida, the serious-delinquency rate in Houma-Thibodaux remained above that of Louisiana’s and was double the level seen in the months prior to the COVID-19 pandemic.

In the span of six weeks in 2020, hurricanes Laura and Delta made landfall just a few miles apart in the Lake Charles metro area, together taking dozens of lives and decimating southwest Louisiana. Similar to Houma-Thibodaux’s experience, Lake Charles’ monthly transition rate from current to delinquent mortgage status jumped from 1% prior to Laura to 8% after. While the effect on the current-to-delinquent transition was temporary, it had longer-term consequences for many homeowners.

The serious-delinquency rate in Lake Charles was below that of Louisiana as a whole prior to the pandemic. It rose at a similar pace as the rest of the state in the early months of the pandemic, but then moved much higher after Laura and Delta struck. As the chart on this page shows, it took about 12 months for the serious-delinquency rate in Lake Charles to return to the level for all of Louisiana.

The Houma-Thibodaux and Lake Charles economies had already been hurt by a drop in oil prices during the early months of the COVID-19 outbreak. With the additional strain of natural disasters, home prices were slow to recover and rent prices weakened as workers and families relocated. According to the CoreLogic Home Price Index, home prices in these two metros rose by 12% from March 2020 to March 2022, compared with a 19% gain for Louisiana and a 34% gain for the U.S. The home-price increases in Houma-Thibodaux and Lake Charles also were less than the two-year inflation rate of 15%.

Natural disasters cause extensive property damage, personal injury, a reassessment of hazard risk and disruptions in local housing markets. Similarly, mortgage delinquency rates spike in the wake of these events, meaning that the prices and availability of shelter also are affected. These impacts are likely to reoccur when the next major tropical cyclone hits the U.S. ●