A truly unprecedented year is now in the books. With that in mind, let’s look ahead at several housing-market trends that are likely to occur in 2021 and beyond.

First, exceptionally low mortgage rates are likely to be around for an extended period. CoreLogic expects that 30-year fixed-rate loans will remain below 3% in the early portion of 2021 and will average about 3.2% over the next three years. This would be nearly a percentage point lower than the 4.1% average from 2010 through 2019, according to historical data from Freddie Mac. These low rates will provide an excellent opportunity for families with good credit to buy or refinance homes.

There were about 20 million outstanding home loans at the start of this year with a contract interest rate of 4% or higher, according to an analysis of CoreLogic and U.S. Census Bureau data, although some borrowers are less likely to refinance because they have a low balance, a recent delinquency or have been in forbearance. But there are still plenty of borrowers who will refinance this year. Expect refinance volume to remain brisk, albeit slower than in 2020.

Second, millennials will substantially boost the demand for housing over the next few years. Looking at the U.S. population, the largest numbers of millennials in 2021 are those ages 29 to 31. The median age of recent first-time buyers is 33, the National Association of Realtors reported, so demographic forces will add an important tailwind to homebuying demand. In fact, from 2021 through 2023, CoreLogic expects home sales relative to the nation’s housing stock, a measure of home “turnover,” to be higher than the average annual turnover rate of the prior two decades.

Millennials and Generation Z will fuel household-formation growth. The number of households are forecast to rise by an average of 1.2 million per year through 2028, or about 1% annual growth, according to the Joint Center for Housing Studies of Harvard University (JCHS). New households will be far more diverse by race and ethnicity. While about two-thirds of U.S. households are white, minorities will account for about three-fourths of the net growth in household formations in the coming years, according to JCHS projections.

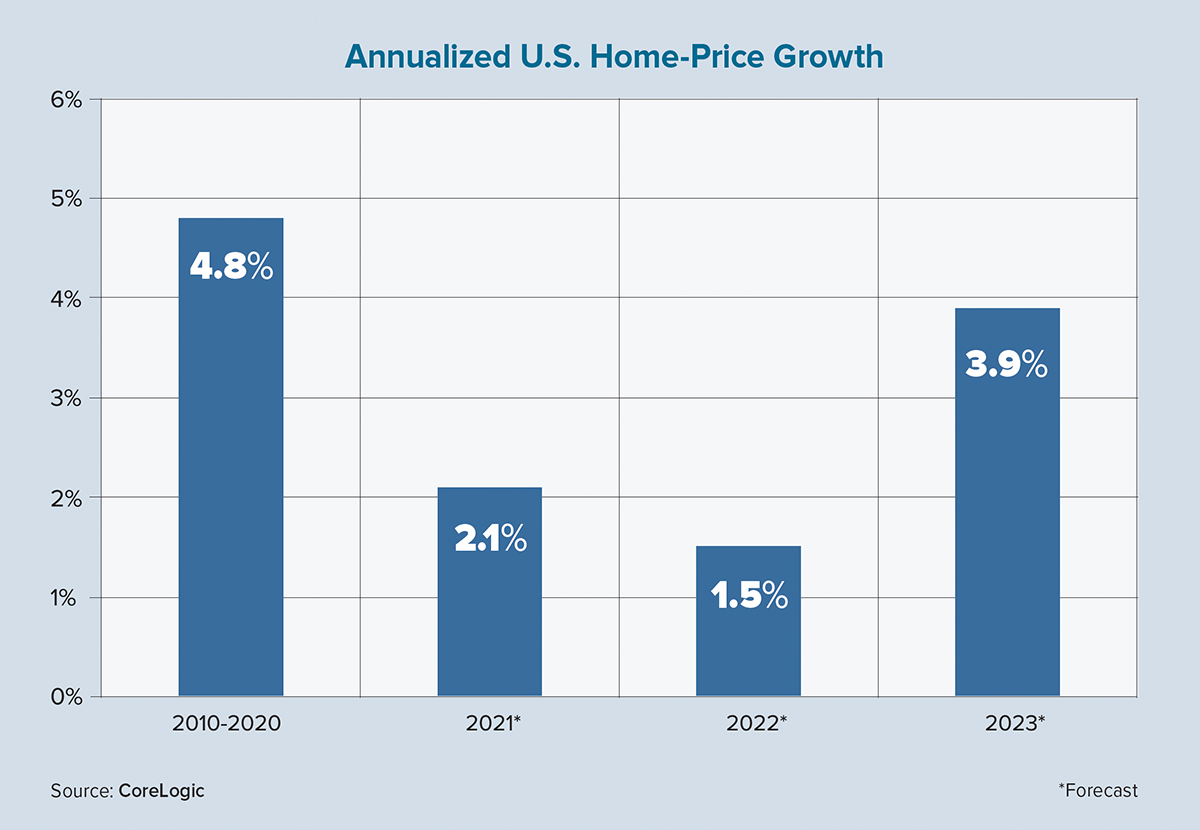

Third, CoreLogic expects home prices to rise in most neighbor-hoods, albeit at a more modest pace than in recent years. U.S. price appreciation is expected to average 2.5% per year over the next three years, compared with 4.8% annual growth during the prior decade, as measured by the CoreLogic Home Price Index. One reason for the slower growth in values is due to an expected increase in for-sale inventory. The pandemic has delayed new-construction efforts and has led many prospective sellers to postpone listings.

The median age of a homeowner is about 57, and with older Americans having greater health risks during the pandemic, many who were contemplating selling their homes have decided to wait. Once the COVID-19 crisis dissipates or a vaccine is widely available, expect to see the number of new and existing homes listed for sale to rise, helping to ease price appreciation.

One caveat: While many neighborhoods likely will see gradual price growth, some metros that have been especially hard hit by the pandemic and the subsequent recession will likely experience price declines. Communities that have a local economy largely based on tourism, hospitality, business travel, entertainment, restaurants or retail are likely to have elevated unemployment rates for an extended period and will face home-price declines. These markets are likely to see an increase in distressed home sales, which will add additional inventory to the local for-sale market.

Low mortgage rates, a growing number of first-time buyers and gradually rising home values are three housing-market trends expected in 2021 and beyond. Best wishes for a healthy and successful new year. ●