The increased frequency and severity of extreme weather events have prompted growing awareness and concern within the commercial real estate industry. Assets once deemed safe from peril now sit precariously in harm’s way.

Acute physical risks such as floods and wildfires, as well as more chronic issues that include water insecurity, have pushed industry stakeholders to demand reliable data and analytics to support economically sound decisionmaking. Data providers have responded by devoting substantial resources toward the science and economics of climate risk.

The economics profession talks at length about expectations and uncertainty. In a traditional market analysis, a cost-benefit approach is used to determine the decisionmaking process of the market participants, which will then lead to a particular market outcome. In the analysis, the values attached to costs or benefits are typically expected values — meaning that there is uncertainty present in the analysis.

Economists deal with this uncertainty by attaching reasonable and defensible probabilities to particular outcomes, thus creating a weighted distribution of outcomes which can then be combined and turned into an expected value. This procedure is currently being conducted in the commercial real estate industry as it relates to climate risk.

Climate risk introduces doubt directly and separately into the space market, capital market and development market, and it also does so indirectly through the natural interactions of the three markets. In the space market, tenants may begin to act on fear caused by the uncertainty of a future event or frustration in having to evacuate their property.

This additional climate change-related cost will reduce demand for spaces in certain areas deemed at risk. Lenders and investors in the capital markets may require a higher rate of return to do business in these same areas. Likewise, potential buyers may stay on the sidelines. And finally, developers could feel the crunch of increased red tape and material costs.

If any or all of these changes happen to existing assets or planned assets in certain markets, a new equilibrium will occur. This likely means an environment with lower rent and occupancy rates, decreased transaction volumes and property values, and slower inventory growth.

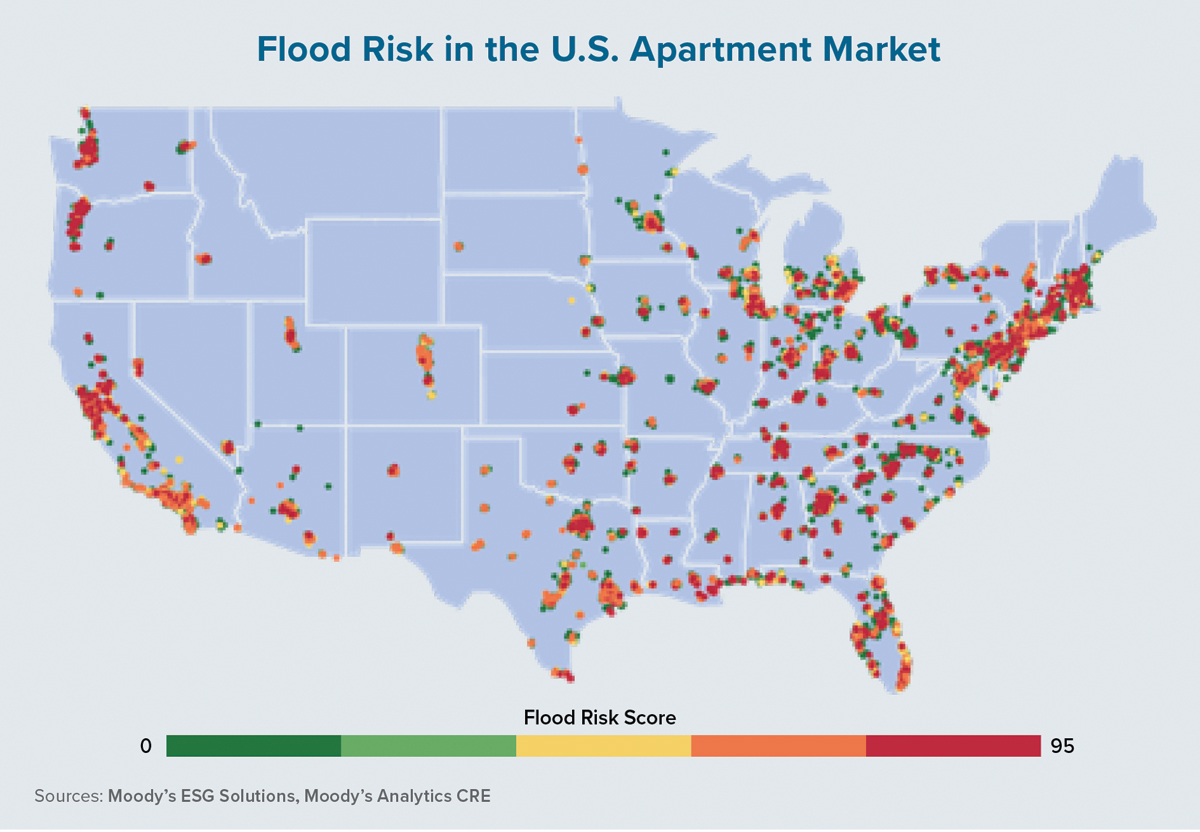

The above theory is all quite pessimistic, but is there room for nuance? We believe so. For one, if there is migration away from risky areas, low-risk areas are likely to benefit. This is true at both a regional and parcel level. For instance, even within flood-prone submarkets, there are vastly different risk levels for different properties, and we find emerging evidence that supports variation in performance metrics across these properties.

Second, some of these parcels of land may be so valuable that lenders, developers and tenants will still find that the cost-benefit analysis points to strong development opportunities. In these situations, any existing or potential tenants may be willing and able to pay for the necessary costs of construction or renovation. This may actually result in higher property values and more exclusive neighborhoods in at-risk but otherwise desirable locations. Local governments also are likely to work hard to provide remedies as they do not want to lose portions of their tax base.

Lastly, the emergence of high-quality data and analytics can help to reduce any risk premiums built into lending or insurance practices. The simple fact that market participants have the tools to understand the true levels of risk and what they actually mean for asset performance means that they are more likely to have the needed transparency for making better and more efficient choices. This should create greater liquidity and free up capital even in some areas deemed at risk.

In sum, the commercial real estate industry has awakened itself to climate risk. This topic finds its way to the top of the agenda in the vast majority of meetings between data analysts and industry stakeholders. There is a general acceptance that assets are at risk and regulations are coming. Reducing the uncertainties that surround these issues through the use of quality data and analytics is vital for allowing the industry to do what it does best — build wisely and efficiently. ●