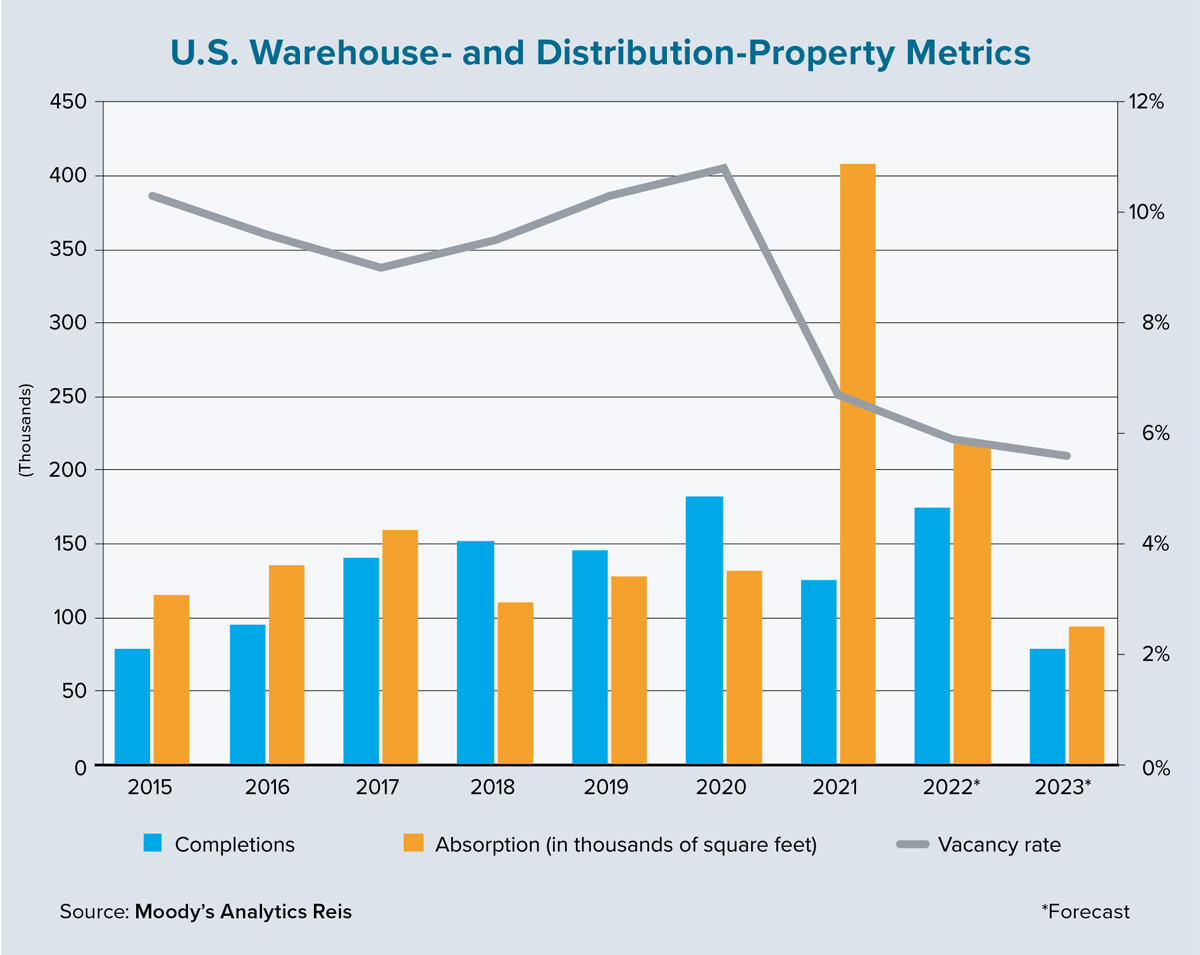

Industrial assets — whether it’s warehouse and distribution space or flex properties designed for research and development — have been the darling of commercial real estate over the past two years, if not longer. Record rent growth has only been eclipsed by record occupancy gains. Capitalization rates have compressed, developers can’t build fast enough to keep up with demand and mortgage brokers have stayed incredibly busy financing these types of properties.

But is the tide starting to shift? Or even worse, should the word “bubble” be mentioned? While the baseline forecast for the industrial sector from Moody’s Analytics Reis remains upbeat (annualized rent-growth rates of 4% to 5% are expected over the next few years), downside risk may be growing as both macro and microeconomic pressures build.

First off, the risk of an economic slowdown or mild recession is increasing. First-quarter 2022 real gross domestic product declined at a 1.4% annual clip. While it’s true that much of this was due to decreases in net exports and federal government spending, markets were rattled and even the most optimistic economists are now placing nontrivial odds on a recession. With interest rates rising, it is likely that the U.S. economy will experience at least a moderate decline in consumer and business spending, which in the past have been highly correlated with industrial-sector performance.

Additionally, recent data supports conflicting performance on the manufacturing and industrial-production front, which are closely tied to industrial real estate. On one hand, the May 2022 release of the Empire State Survey of Manufacturing showed a plummeting business-conditions index in New York state, driven by fewer new orders. On the other hand, the 1.1% gain in U.S. industrial production from March to April was a strong positive. But given that the first metric is a bit better leading indicator of future activity, there are at least some headwinds for near-term space demands within the sector.

The second overarching concern stems from the potential for overexuberance. It is possible that real estate investors and logistics companies overestimated the expected long-term growth of the fundamentals that prompted such enthusiasm for industrial real estate. Much has been written about the growth of e-commerce as a major tailwind for the sector, but recent data suggests that the COVID-19 pandemic’s positive shock to e-commerce was more transitory than permanent.

May 2022 figures from the U.S. Census Bureau showed that the online share of all retail sales has continuously declined from its Q2 2020 peak of 16.4% to only 14.3% at the end of Q1 2022. Although the latter figure is a 240-basis-point increase from Q1 2019, it also is a reversion back to the pre-pandemic growth path and is not the trend of acceleration many had anticipated.

Furthermore, while consumers keep spending during this period of elevated inflation, a significant share of the spending has gone to food-services and drinking establishments. In fact, sales in this retail category grew by nearly 20% year over year in April 2022 while overall spending was up about 8%. Service-sector and restaurant spending certainly has links to industrial real estate, but the positive effects are likely lower in scale than sales of durable and nondurable goods.

Lastly, even Amazon has admitted to overextending itself in the most recent push for space. As CEO Andy Jassy said in a recent earnings call, Amazon is “no longer chasing physical or staffing capacity.”

What do these concerns — combined with already record lease rates and property prices — mean for industrial real estate stakeholders? Moving forward, it is likely that some of the excitement for this sector will subside, and that certain acquisition and development deals will garner an additional layer of scrutiny. But this is not necessarily a bad thing for the overall health of the sector. Slightly softer demand, along with delays in speculative inventory growth due to supply chain issues and higher interest rates, may serve to prevent a bubble.

Overall, the long-run fundamentals are solid for industrial real estate. The U.S. logistics network still needs to evolve and grow to prevent future supply chain issues, but competition within retail will only serve to promote development that will reduce shipping times. Toss in a movement back toward just-in-case inventory management, along with a revived domestic advanced manufacturing industry, and the prospects for long-term growth in industrial real estate look bright. ●