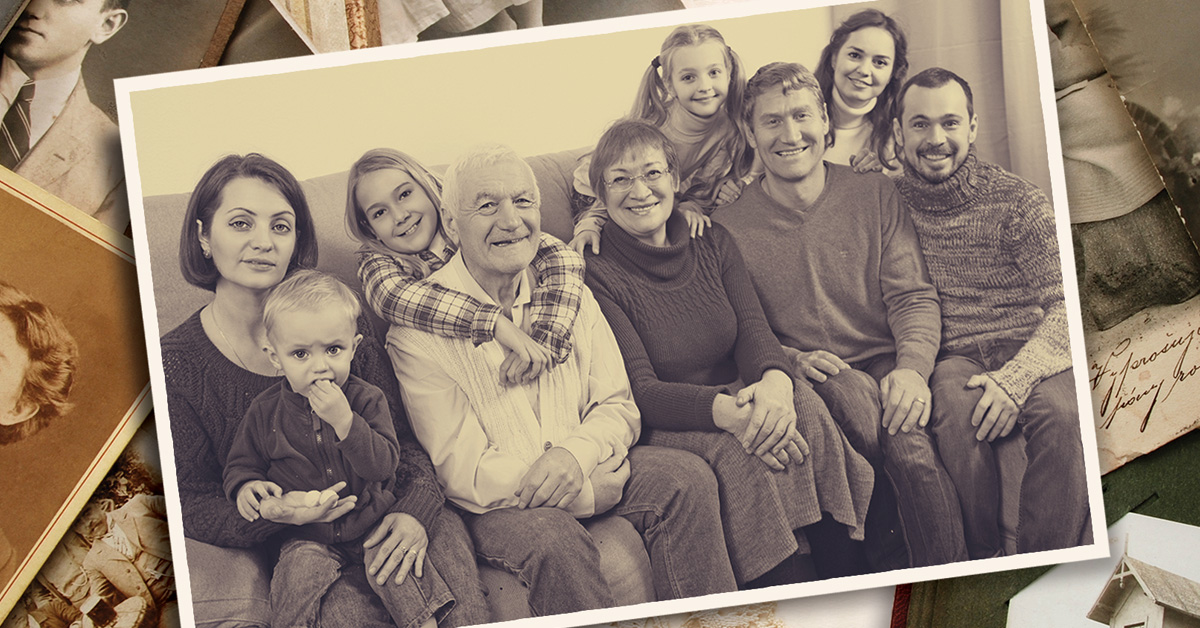

In the bygone days of the early 1900s, it was more common than not to have multiple generations living under one roof. It wasn’t only the family farm that was passed through the generations with children, parents and grandparents living together. This was the norm everywhere. The idea conjures images of children coming home from school to see grandma tending to her garden or grandpa snoozing in the recliner. The family gathered around the dinner table to chat about the day. Today you can leverage this nostalgia to answer some contemporary housing challenges.

What are some of the advantages of multigenerational housing? Well, when a family chooses multigenerational housing, they can provide comfort to aging parents, delay costly nursing home care or help a young family care for children while offsetting child care costs.

Being open to multigenerational housing can answer needs for a variety of family situations. Maybe it’s a relative who needs a home while attending an out-of-state college or a distant relation staying for a few months while visiting from another country.

This option also is a good way to help adult children avoid paying high rents while they save toward a downpayment on a future home purchase. Snow-bird retirees who live for part of the year in multigenerational housing are able to maximize their independence while maintaining precious connections to their family.

Multigenerational housing does not need to be a permanent arrangement, but it can be one if it suits the needs of the families involved. Mortgage originators should not only mention this as an option but offer creative financing that could make this a possibility.

Emerging trend

To this point, why aren’t trusted housing advisers openly suggesting this to their clients? The idea that an adult child must vacate the family nest and fly out on their own is misguided. For example, the Pew Research Center last year reported that nearly four in 10 men between the ages of 25 to 29 live with older relatives.

This way of life in the U.S. has grown sharply over the past five decades with no signs of peaking. Pew reported in 2016 that 20% of the country lives in multigenerational households. That’s nearly the same share as in 1950, when 21% of Americans lived in multigenerational homes. The difference is that in 1950 these living arrangements included 32.2 million people. In 2016, 64 million Americans lived in multigenerational households. Some of this can be attributed to growing racial and ethnic diversity in the country, but it’s not the sole reason.

The reasons why this make sense are as numerous as family living arrangements. For instance, a family could be modifying their home to accommodate an older generation. The payoffs can be peace of mind coupled with strong bonds between children and grandparents.

Early on, grandparents can help with after-school child care, allowing their kids to pursue career goals. Later on, the grandparents can have a place to stay without the worry of home maintenance. They are free to enjoy their senior years as they see fit in a safe environment. A home renovation mortgage can provide financing in these cases.

Evolving families

Maybe a job situation is the impetus for generations living together. Let’s say a woman is an only child and her father passes away, leaving behind an elderly mom. Then the woman’s husband gets a new job and they move across the country, leaving the woman in a bind. How does she care for her mom in her later years while living so far away?

The answer may be for the mom to move in with the couple. They can sell each of their homes and pool equity together to buy a new house with a mother-in-law suite in a new state. No one is left behind and the elderly mother is able to begin her independent retirement years surrounded by family with few property responsibilities. Purchase programs for existing homes or newly built construction can be attractive for borrowers like this family.

With home prices as high as they are, many young couples are choosing to start married life living with one of their parents. They’re doing this in order to save as much as they can toward a downpayment for a home. This is usually a short-term situation, but with the ongoing housing shortage, these stays can shift from a matter of months to a few years. Patiently waiting for the right house at the right price, they may even start their own family.

Three generations deep, there will come a day in the near future for these young couples to move out, but as long as the arrangement is amicable, they’ll save for that first-time home purchase. They’ll be in need of a mortgage adviser to help them when that time comes.

Financial incentive

Although providing care (either child care or elder care) is a driving reason for multigenerational housing, financial reasons also are huge factors in making this choice. If two can live as cheaply as one, then what’s the payoff for adding a few more to the mix? Multigenerational living arrangements can be the difference between living in poverty and not.

Multigenerational housing is one way for people to escape paying rent to a landlord or making payments to an assisted-living facility. Imagine how much equity a family can build if they’re using the extra money that would have gone to a rental or care facility to pay off the mortgage on the family’s primary home.

Oftentimes, multigenerational families will need extra space. And that’s where an accessory dwelling unit (ADU) may make sense. An ADU is a small dwelling that is either attached to a typical single-family home or a separate unit located on the same grounds. More cities and counties are allowing this type of construction to deal with housing shortages. ADUs can be financed with a cash-out refinance, renovation refi or a construction-to-permanent loan option to make this dream a reality.

A close cousin of multigenerational housing is Fannie Mae’s Family Opportunity Mortgage. This loan product allows clients to get a mortgage for their elderly parents or a disabled adult child. Your clients qualify for the mortgage, but the loved ones occupy the home.

Many families who are on the threshold of sending a child to college find that on- and off-campus housing can be more costly than the tuition bill. Smart spending could come in the form of an owner-occupied small home purchase where the college student is the occupant but the parents are on the mortgage note.

Qualified borrowers can leverage standard purchase or refinance options across Fannie Mae, Freddie Mac and Federal Housing Administration products. The college student attends the university as a commuter and once graduation has commenced — provided the market has grown and the home was maintained — there should be a nice return on investment once the property is sold. There can be roommates to generate rental income, too, if that’s a plan the parents and student want to explore.

● ● ●

Mortgage professionals should be mindful of the changing needs of their clients. Once the loan closes, you owe it to your borrowers to periodically check on them and make sure the home still fits. If there is a change in circumstances, you can calm their stress by offering lending solutions that help them maximize the equity they’ve built so they can refinance, make modifications and continue enjoying the comfort of their home.

If a move is needed to accommodate their family changes, you have the opportunity as their trusted mortgage adviser to reassure them with existing home and new construction purchase options. It’s almost like you’re a member of their family. ●